As climate change reshapes the U.S. housing market, many homebuyers and homeowners in California and the Bay Area are reevaluating their options. With insurance premiums skyrocketing, extreme weather events increasing, and property values shifting, the once predictable patterns of migration and investment have been fundamentally disrupted. According to the 12th National Risk Assessment: Property Prices in Peril, climate risk is now a central driver of real estate trends across the country. This article explores some of the best and worst places to move based on climate resilience and affordability, with a special focus on California and Bay Area homeowners.

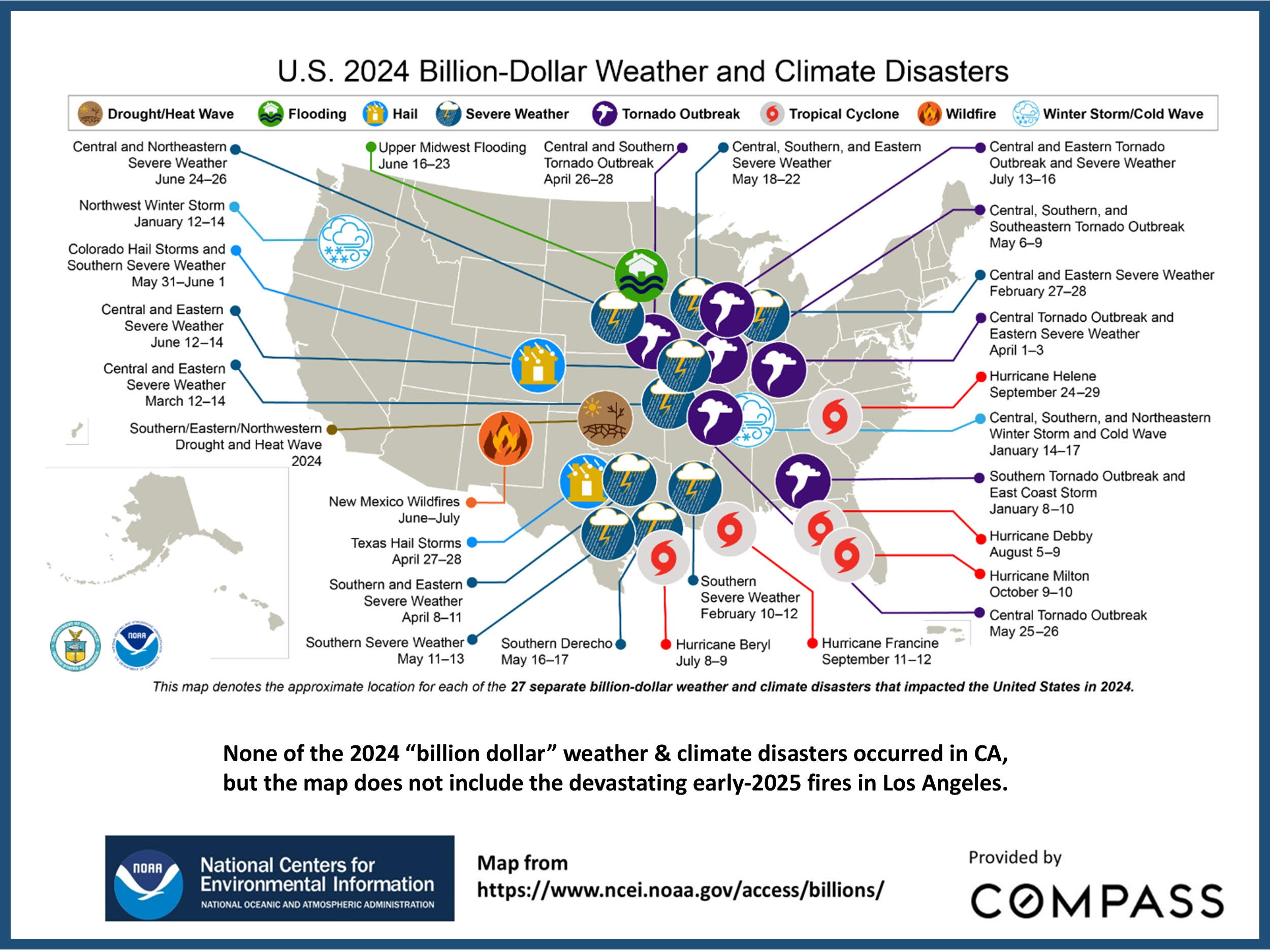

The 12th National Risk Assessment highlights the profound financial impact climate change will have on U.S. real estate, projecting that over $1.47 trillion in property value losses will occur by 2055 due to rising insurance costs, increased natural disaster exposure, and shifting consumer demand. Homeowners in high-risk areas, particularly in the Sun Belt and coastal regions, are seeing higher costs of ownership and diminishing desirability, leading to widespread devaluation of real estate assets.

As insurance markets price in climate risks and extreme weather events become more frequent, entire neighborhoods are facing economic decline, with properties in flood-prone, wildfire-prone, and hurricane-exposed regions experiencing the most significant downturns. This report underscores the urgency for homebuyers and investors to factor climate resilience into their real estate decisions, as the financial landscape of homeownership continues to shift in response to these evolving risks.

How Climate Change Is Reshaping Real Estate Markets

The 12th National Risk Assessment underscores a few critical ways in which climate risk is disrupting the housing market:

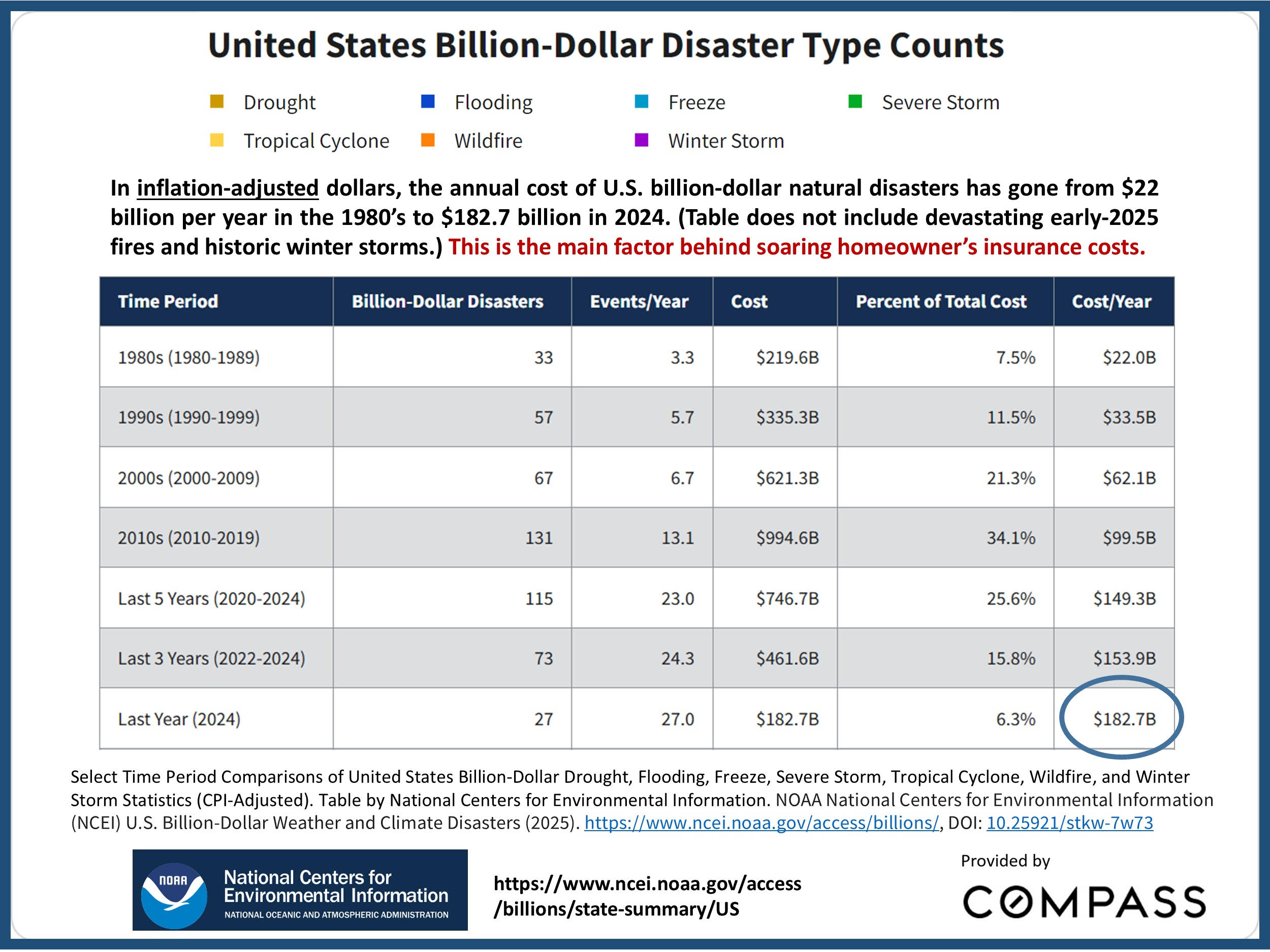

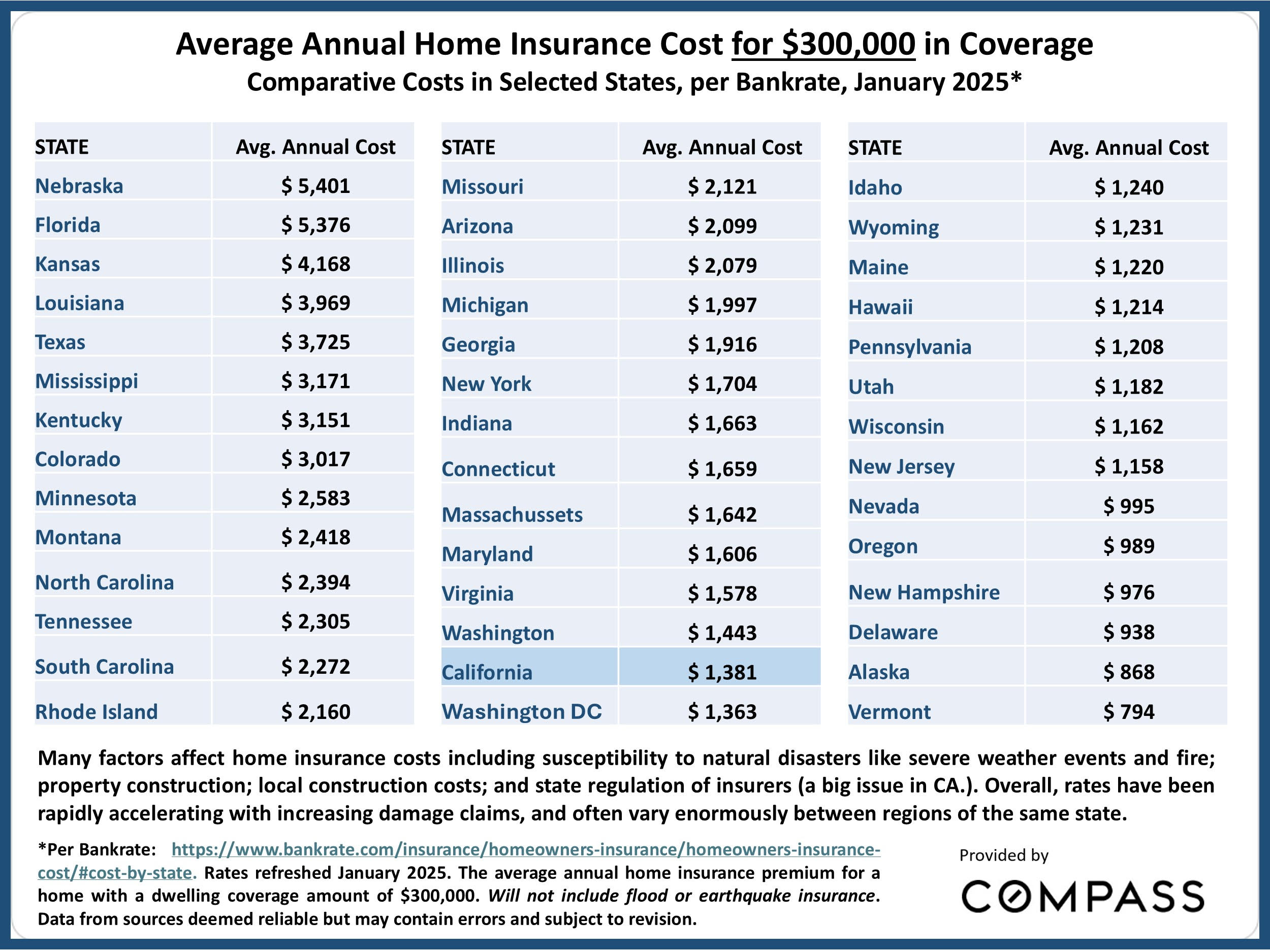

- Insurance Premiums Are Skyrocketing: In many high-risk areas, insurance costs are rising faster than mortgage payments. From 2013 to 2022, insurance as a percentage of mortgage payments more than doubled, climbing from 7-8% to over 20%.

- Climate Migration Is Accelerating: Over 55 million Americans are expected to relocate to lower-risk areas by 2055, with 5.2 million moving in 2025 alone.

- Property Values Are Declining in Risky Areas: By 2055, climate risk is projected to cause $1.47 trillion in net property value losses across 70,026 neighborhoods, accounting for 84% of U.S. census tracts.

- The Sun Belt’s Growth Is Slowing: California, Texas, and Florida have absorbed over 40% of the nation’s $2.8 trillion in natural disaster costs since 1980, making these states particularly vulnerable to rising insurance costs and declining desirability.

Given these trends, let’s explore the worst and best places to move for Bay Area homeowners, based on climate resilience and home prices.

The Worst Places to Move If You’re Concerned About Climate Change and Home Prices

As climate-related risks escalate, certain regions in the U.S. are becoming increasingly undesirable for homeowners due to the combined pressures of rising insurance premiums, frequent natural disasters, and property devaluation. The worst places to move include areas facing severe hurricanes, wildfires, floods, and extreme heat. Homeowners in these locations are seeing higher costs of ownership due to expensive insurance policies, property damage, and infrastructure stress. This section highlights some of the most vulnerable areas, explaining why these regions may not be ideal for long-term homeownership and investment.

Florida (Miami, Tampa, Jacksonville)

- Insurance premium increases: Miami (322%), Jacksonville (226%), Tampa (213%)

- Climate risks: Hurricanes, sea-level rise, extreme heat

- Key concern: The combination of rising insurance premiums and increasing exposure to hurricanes makes Florida a financial risk for homeowners. Many insurers have already exited the market, leaving homeowners with skyrocketing costs.

Houston, Texas

- Projected days of extreme heat annually: 85+

- Climate risks: Hurricanes, flooding, extreme heat

- Key concern: Despite economic growth, Houston remains highly vulnerable to climate-related flooding and heat waves. Home insurance rates have surged 40% in recent years, with flood insurance premiums nearly doubling under FEMA’s Risk Rating 2.0.

Southern California (Los Angeles, San Diego, Orange County)

- Climate risks: Wildfires, droughts, rising insurance costs

- Key concern: Wildfire risk has driven insurance companies to either leave the market or drastically increase premiums. In some high-risk areas, homeowners are left with limited and expensive coverage options.

New Orleans, Louisiana

- Insurance premium increase: 196%

- Climate risks: Hurricanes, sea-level rise

- Key concern: New Orleans remains one of the most flood-prone cities in America. With continued sea-level rise and increasingly intense hurricanes, property values are at significant risk.

Sacramento, California

- Insurance premium increase: 137%

- Climate risks: Wildfires, extreme heat, drought

- Key concern: While Sacramento has long been considered a more affordable alternative to the Bay Area, its increasing exposure to wildfires and rising insurance costs make it a less attractive option.

The Central Valley

California residents thinking about relocating inland should be aware that Climate abandonment impacts are projected to be most severe in California’s Central Valley. Here are some eye-popping nuggets from the report:

- Fresno County projected to lose 48.5% of its population by 2055

- Sacramento County (Sacramento, Roseville, Folsom) projected to lose 27.8% of its population by 2055

The Best Places to Move for Climate Resilience and Stable Home Prices

While many regions are facing increasing climate risks and declining property values, some areas stand out as safer, more resilient places to live. These locations offer lower exposure to natural disasters, more stable insurance markets, and long-term affordability. Homebuyers seeking to minimize climate-related financial risks should consider these regions, which are gaining popularity among climate-conscious movers. This section highlights some of the best places to relocate for long-term stability and investment security.

1. Pacific Northwest (Seattle, Portland, Spokane)

- Climate benefits: Milder temperatures, fewer extreme weather events

- Key advantage: Lower risk of hurricanes, wildfires, and extreme heat makes this region one of the safest bets for long-term home value retention.

2. Great Lakes Region (Minneapolis, Madison, Grand Rapids)

- Climate benefits: Access to freshwater, fewer natural disasters

- Key advantage: As climate migration reshapes the U.S., the Great Lakes are emerging as a climate refuge due to stable home prices and lower insurance risks.

3. Northeast (Burlington, VT; Pittsburgh, PA; Albany, NY)

- Climate benefits: Lower risk of wildfires and hurricanes

- Key advantage: Rising interest in smaller, more climate-resilient cities has led to an influx of new residents, boosting local economies without dramatically increasing insurance costs.

4. Asheville, North Carolina

- Climate benefits: Lower wildfire and hurricane risk than other Southern cities

- Key advantage: A desirable mix of affordability, scenic landscapes, and climate resilience makes Asheville an increasingly popular destination.

5. Colorado Springs, Colorado

- Climate benefits: Less wildfire exposure than other parts of the state

- Key advantage: While Colorado as a whole has seen wildfire-related insurance issues, Colorado Springs remains relatively insulated from the worst climate risks.

What Bay Area Homeowners Need to Know

As climate risks intensify, Bay Area homeowners must stay informed about how environmental changes impact property values, insurance costs, and long-term livability. Wildfire risk remains a top concern, particularly in hillside communities and areas near open spaces, where stricter building codes and defensible space requirements are becoming the norm. Rising sea levels threaten homes in low-lying coastal regions, prompting cities to invest in shoreline protections that could lead to new fees or assessments for homeowners. Meanwhile, the ongoing home insurance crisis means that properties in high-risk zones may face skyrocketing premiums or difficulty securing coverage altogether. Understanding these factors is crucial for current and prospective homeowners, as climate resilience is increasingly shaping buying decisions, financing options, and future resale potential in the Bay Area market, and far beyond.

Here’s what you need to keep in mind:

1. Coastal Risk Is Growing

Rising sea levels are a concern for properties in low-lying areas like Foster City, Alameda, and parts of San Francisco’s Marina District. Homeowners in these areas should consider flood insurance, even if they’re not in a designated flood zone.

2. Insurance Costs Are Climbing

California’s insurance market is undergoing major shifts. Many insurers are pulling out of high-risk areas, forcing homeowners into the expensive California FAIR Plan, which provides last-resort coverage at higher rates.

3. Wildfire Risk Is a Major Concern

If you own property in the Santa Cruz Mountains, Napa, or Sonoma, be aware that wildfire risk assessments are affecting both insurance availability and property values.

4. Home Prices May Be Affected by Climate Migration

As people leave high-risk areas for safer regions, some Bay Area properties – especially those more prone to flooding and wildfire – may see declining demand, which will ultimately result in lower property values – possibly much lower. Keeping up with climate risk reports and market trends is essential for long-term financial planning.

Identifying Areas with High Climate Change Resilience

Investing in real estate with an eye toward long-term appreciation requires careful consideration of climate risks. Regions less susceptible to extreme weather events and environmental changes are often more likely to experience stable or appreciating property values. If you’re looking to identify which areas these may be, it’s important to consider what contributes to climate resilience.

Factors Contributing to Climate Resilience

- Geographic Location: Inland areas at higher elevations are generally less vulnerable to sea-level rise and coastal storms.

- Economic Diversification: Regions with diverse economies are better equipped to withstand and adapt to climate-related challenges.

- Stable Water Supply: Regions with ample freshwater access and sustainable water management are better equipped to handle droughts.

- Infrastructure and Planning: Cities investing in resilient infrastructure and sustainable urban planning are more likely to maintain property values. Areas investing in smart grids, renewable energy sources, and decentralized power infrastructure are less likely to experience energy disruptions.

Example of Climate-Resilient Cities in the U.S.

- Madison, WI (Low natural disaster risk, strong infrastructure)

- Minneapolis, MN (Diverse economy, sustainable urban planning)

- Asheville, NC (Moderate climate, high community engagement)

- Denver, CO (Elevation advantage, climate adaptation initiatives)

When considering real estate investments, it’s crucial to assess both the economic prospects and the climate resilience of the area. Engaging with local planning resources and staying informed about regional climate adaptation initiatives can provide valuable insights for making informed decisions.

Final Thoughts

For California and Bay Area homeowners, understanding the interplay between climate risk and home prices is more crucial than ever. Whether you’re looking to relocate or protect your current investment, staying informed about insurance trends, migration patterns, and property value shifts will help you make smarter real estate decisions. While some areas remain high-risk, others present opportunities for stability and long-term growth. Choosing wisely now can safeguard your financial future in an increasingly unpredictable climate landscape.

Your Neighbor Sold their House too Cheap!

Terrific Sunnyvale Homes for Sale

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25