Hey everyone! Welcome to my September 2025 Silicon Valley real estate market update. If you’ve been following the market closely—or just trying to figure out what’s happening with home prices in the South Bay—you’re probably noticing some interesting patterns emerging. We’ve got the August numbers in from both Santa Clara and San Mateo counties, and there’s quite a story to tell.

The Big Picture: Prices Hold Steady, But Markets Are Shifting

Let’s start with the headline numbers because they tell us where we are, but more importantly, they hint at where we might be headed.

In Santa Clara County, the median home price hit $1.88 million in August. Now, that might sound astronomical if you’re coming from anywhere else in the country, but for those of us tracking this market, it’s actually been remarkably stable—unchanged from July. What’s interesting is that we’re still seeing about 3% growth year-over-year, which suggests the market has found some equilibrium after the wild swings of recent years.

San Mateo County tells a slightly different story. Median prices there climbed to $1.9 million, up about 1.1% from July and nearly 7% compared to last August. That’s a stronger price performance than Santa Clara, which makes sense when you consider San Mateo’s proximity to San Francisco and the Peninsula’s continued appeal to tech workers.

But here’s what’s really catching my attention: homes are taking longer to sell. In Santa Clara County, the median days on market jumped to 13 days—that’s up 30% from last year. San Mateo County saw a similar trend with 14 days on market, up nearly 8% year-over-year. Now, 13-14 days is still incredibly fast by national standards, but for Silicon Valley, this represents a meaningful shift toward a more balanced market.

The Per-Square-Foot Story

When we look at price per square foot, we get a clearer picture of actual value trends. Santa Clara County hit $1,043 per square foot in August, up 5% from July and 4% year-over-year. San Mateo County reached $1,156 per square foot, essentially flat month-over-month but up 4% annually.

These numbers matter because they strip away some of the noise from varying home sizes and give us a cleaner read on underlying value trends. The fact that both counties are showing solid year-over-year gains in per-square-foot pricing suggests that despite some market cooling, fundamental demand remains strong.

Sales Volume: A Tale of Two Counties

Here’s where things get interesting. Santa Clara County saw 724 homes sell in August, which is actually up 1.6% from July and more than 5% from last year. San Mateo County had 313 sales, up 14% from July and almost 6% year-over-year.

This increased activity is happening despite—or perhaps because of—falling mortgage rates. More on that in a moment, but it’s worth noting that we’re seeing buyers come off the sidelines as financing becomes more affordable.

Your Neighbor Sold their House too Cheap!

Inventory: Still Tight, But Improving

One of the most persistent features of the Silicon Valley market has been severely constrained inventory. We’re still in that mode, but things are loosening up slightly. Santa Clara County had about 1.3 months of inventory in August, up 16% from July. San Mateo County had 1.5 months, up 3% month-over-month.

For context, a “balanced” market typically has around 6 months of inventory, so we’re still operating in what’s clearly a seller’s market. But the direction is encouraging for buyers who’ve been frustrated by the lack of options.

The condo market in Santa Clara County shows similar patterns, with 563 condos for sale as of early September—below the long-term average of 757 since 2000, but with days of inventory improving from 77 to 68 days.

The Mortgage Rate Factor: A Double-Edged Sword

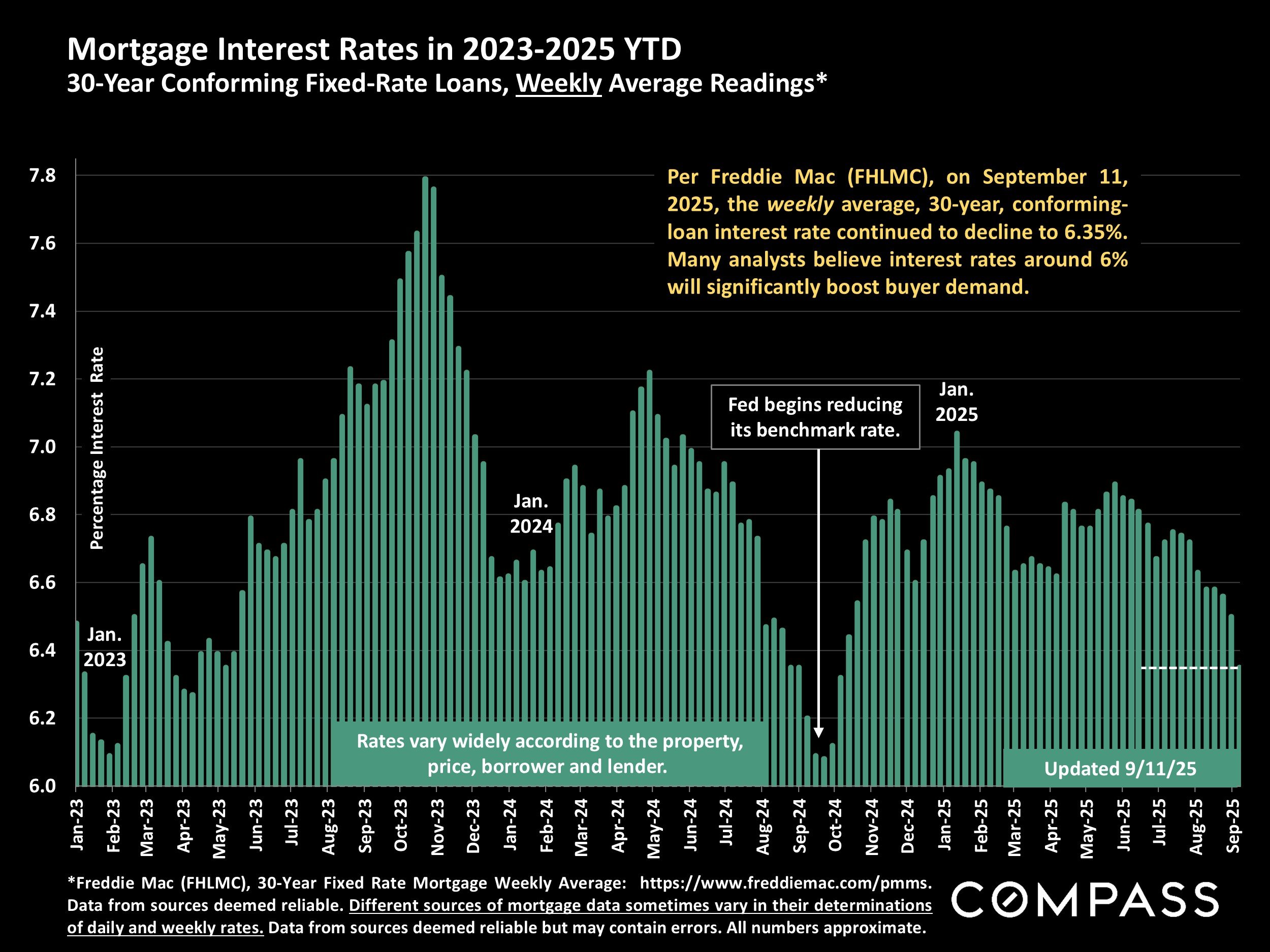

Now let’s talk about the elephant in the room: mortgage rates and what they mean for this market. As of September 11th, 30-year fixed rates averaged 6.35%—the lowest we’ve seen since October of last year. For many potential buyers, this represents meaningful relief after rates peaked above 7% earlier in 2024.

But here’s the thing that’s keeping me up at night: rates aren’t falling because the economy is strengthening. They’re falling because it’s weakening. National job growth slowed dramatically to just 22,000 new positions in August, and unemployment has climbed to 4.3%.

For Silicon Valley real estate, this creates a fascinating paradox. Lower rates should theoretically bring more buyers into the market and support prices. But if the job market continues to soften—especially in tech—we could see demand cool even as financing becomes more affordable. It’s a delicate balance, and frankly, it’s what makes this market so hard to predict right now.

Tech Sector Headwinds: The Reality Behind the Headlines

Speaking of tech jobs, we can’t ignore what’s been happening in Silicon Valley’s core industry. The San Francisco-San Mateo area suffered a net loss of 5,400 tech jobs over the first four months of 2025, and over 2,086 layoffs were disclosed in Bay Area tech companies just in the first five weeks of 2025.

This isn’t just abstract economic data—these are real people who drive demand for $1.8 million homes. While major companies like Oracle continue announcing layoffs, including 187 workers from their former Redwood City headquarters, the market seems to be absorbing these job losses better than many predicted.

Why? A few reasons. First, many laid-off tech workers are finding new positions relatively quickly, often at higher salaries. Second, the people getting laid off often have substantial equity from previous stock grants, giving them financial cushion. And third, the sheer wealth accumulated during the pandemic boom years has created a buffer that’s still supporting home purchases.

Corporate Real Estate: Mixed Signals

Here’s where the story gets really interesting. While individual tech workers face uncertainty, the big corporations are still betting heavily on Silicon Valley real estate. Apple dropped $365 million on the Mathilda Campus in Sunnyvale this year, bringing their total Bay Area acquisitions to around $900 million. Nvidia picked up another Santa Clara office complex on Walsh Avenue for $123 million.

These massive investments send a clear signal that the region’s biggest players still see Silicon Valley as central to their long-term strategy. But it’s creating an interesting dichotomy: corporate demand remains strong even as office vacancy rates hit concerning levels. Sunnyvale, for instance, is dealing with roughly 18% office vacancy, and new office development across the Valley is at a 12-year low.

What does this mean for housing? Well, if Apple and Nvidia are investing nearly a billion dollars in local real estate, they’re presumably planning to employ people in those buildings. That should support residential demand over time, even if the immediate picture looks choppy.

The International Factor: A Growing Influence

One trend that’s been flying under the radar is the surge in international buyers. A recent CBS News analysis found that foreign buyers are increasingly active in Bay Area real estate, with Chinese investors leading the pack, followed by buyers from Canada, Mexico, India, and the UK.

Nationally, foreign buyers purchased about 78,100 properties worth $56 billion between April 2024 and March 2025—a 44% year-over-year increase. In California, international buyers are particularly drawn to Silicon Valley, seeing opportunities in both business investments and attractive housing values relative to their home markets.

This matters because it adds another layer of demand that’s somewhat insulated from local employment trends. Even if tech jobs soften, international cash buyers can help support the high end of the market.

Consumer Sentiment is Weak, But Less So For Buyers

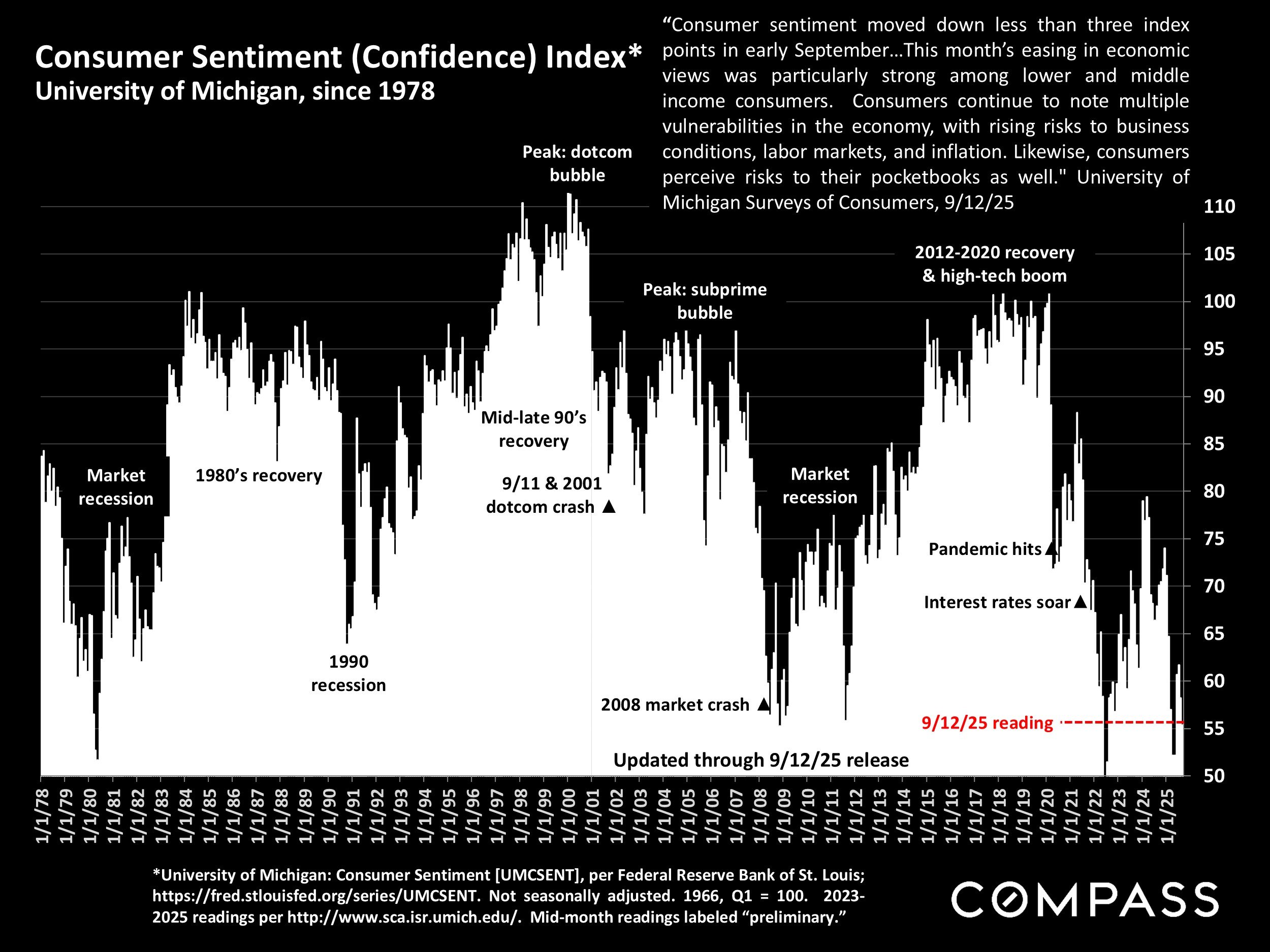

Current consumer sentiment presents a mixed but cautiously optimistic picture for Silicon Valley real estate. National consumer confidence has declined to 55.4 points in September from 58.2 in August, while the LSEG/Ipsos Primary Consumer Sentiment Index dropped to 52.4, down 1.1 points from the previous month. However, housing-specific sentiment tells a more nuanced story, with Fannie Mae’s Home Purchase Sentiment Index at 71.4 in August, suggesting consumers remain relatively optimistic about real estate despite broader economic concerns.

In Silicon Valley specifically, this sentiment divergence is particularly pronounced—while companies seeking to recruit top talent are increasingly looking to grow in areas where employees have more confidence they can afford to buy a house, the region’s established residents and investors appear to be adapting to the new reality of higher prices and rates. California consumer confidence has actually hit a 6-month high, rising 18% since April’s recent low, which bodes well for continued housing demand. For the Silicon Valley market, this suggests that while buyers may be more selective and price-conscious than during the pandemic boom, the underlying demand remains intact, particularly as mortgage rates decline and inventory slowly improves. The key factor will be whether local tech employment stabilizes, as consumer confidence in this market is intrinsically tied to the perceived security of high-paying technology jobs that enable people to afford $1.8 million median home prices.

Looking Forward: What to Watch

As we head into the fall selling season, several factors will shape how this market evolves:

Interest Rates: If the Fed continues cutting rates to address economic weakness, we could see mortgage rates drop into the high 5% range by year-end. That would be a game-changer for buyer affordability.

Tech Employment: The next few months will be crucial for understanding whether tech layoffs are stabilizing or accelerating. Companies’ 2026 planning cycles will give us better visibility.

Inventory: Silicon Valley house prices reached their all-time high in Q1 2025, with 64% of houses still selling over list price, but the trend toward longer market times suggests we’re moving toward better balance.

Political Factors: Immigration policy changes could significantly impact both tech hiring and international buyer activity—two key demand drivers for this market.

The Bottom Line

What we’re seeing in Silicon Valley right now is a market in transition. The days of 5-day sales and 20% over asking are largely behind us, but we’re nowhere near a buyer’s market either. Prices remain elevated but stable, sales activity is picking up as rates fall, and inventory is slowly improving.

For buyers, this is probably the best environment we’ve seen in several years. You’ll have more choices, a bit more negotiating power, and better financing costs than we’ve seen recently. For sellers, you can still achieve strong prices, but you’ll need to be more strategic about pricing and presentation.

The wild card remains the broader economic picture. If tech employment stabilizes and rates continue falling, we could see renewed price appreciation by spring. But if job losses accelerate or economic uncertainty deepens, this gradual cooling could become something more significant.

Either way, Silicon Valley’s fundamental advantages—world-class universities, established tech ecosystem, favorable climate, and limited developable land—aren’t going anywhere. This market has weathered plenty of storms over the decades, and while we’re definitely in for some chop ahead, the long-term trajectory still points upward.

That’s your Silicon Valley market update for September 2025. The market is evolving, opportunities are emerging, and as always in this region, staying informed and acting decisively when the right opportunity presents itself will be key to success.

Time to talk to a REALTOR?

Great Santa Clara Homes for Sale

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25